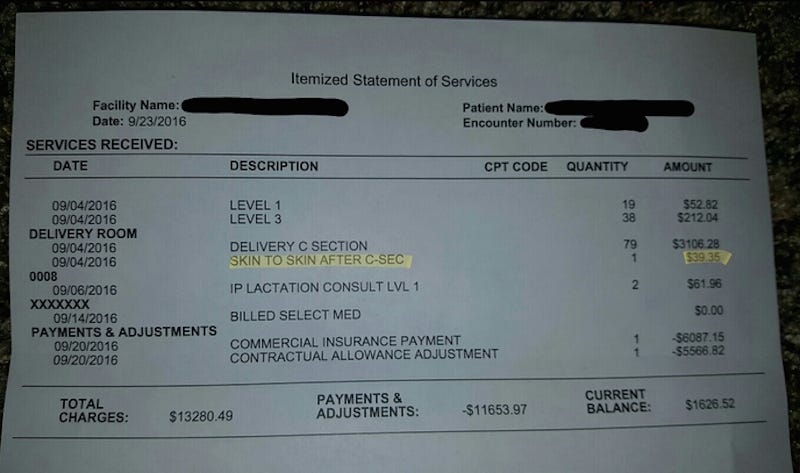

Jezebel reports that a couple was charged $39.95 for holding their baby after a C-section birth:

The story on Jezebel notes that there are the usual host of health-care explanations, the most common being that holding your baby in the ER requires the addition of an extra nurse 'to watch the baby.'

Obamacare was supposed to reduce health care costs; Obama predicted the 'average' family would save $2,500 per year. Years into the program, health care spending continues to rise. While some of the causes are Republican-led states refusing Medicare expansion funds, the fact is costs are rising. Some predictions suggest they will rise by as much as 60 percent over the next 10 years, adding $4,000+ per year to the 'average' bill.

If you are pro-Obamacare, you point out that costs are increasing more slowly: 3-4% per year rather than 4-6% per year prior to Obamacare. The "average" savings works out to $135 per household -- that's $135 less than they would be, if Obamacare hadn't passed.

The White House itself said Obamacare wasn't the most important factor in the slowdown of health care cost increases; the major factor was generally deemed to be The Great Recession: people were too poor to go to the doctor.

Another problem: Deductibles are rising. The National Review, which may not be the least-biased source, aptly described deductibles as the cost of using insurance; premiums are the cost of having insurance, but it's no good if you don't use it. We have a "high deductible" plan: we pay the first $4,000 of all health care each year, which effectively is another $350 or so per month on our health insurance premiums. High deductibles make people question whether they really need to go to the doctor, which may or may not be a good thing. Not going to a doctor at the first sign of a sickness may result in a worse sickness later on. Two years ago, Sweetie got the flu; she didn't go to the doctor right away because she thought it was just a cold. Two days in, we had to take her to the Emergency Room because she'd been unable to hold anything down for two days and was badly dehydrated. The ER doctor said if she'd gone to the doctor earlier he could have given her 'TheraFlu' and avoided much of the trouble. I took two days off of work to watch the kids. I'm salaried, so I didn't lose any money, but that's about 14 billable hours my firm didn't get, and meant that work for my clients was two days behind schedule.

A more reputable source, the New York Times, reported in 2015 that health-care deductibles were rising faster than workers' wages. Industry experts described raising deductibles as the "go to" choice for cost savings: the cost savings are entirely on the employers and the health insurance companies, as there is no way to doublespeak your way into describing higher out-of-pocket costs for a person as a 'cost savings.'

No way, that is, unless you factor in that 40% of people have opted to forego a doctor's visit because of the cost of deductibles, including (in that same NYT article) a woman who won't get an MRI to see if her cancer has come back because of the cost. As deductibles rise, people with chronic conditions (like, say, asthma that requires 8 different daily medications to allow one to breathe) tend to seek care less.

Health insurance companies have seen their profits soar as their business changes. Over the past few years, "Administrative Service Contracts" have been a growth area for insurance companies: under these contracts, the companies negotiate and manage care, but pay no money out of pocket: all costs come from the employer. In some cases, this has doubled the actual out-of-pocket cost when a person goes through "insurance" (ASCs are not "insurance" as people think of it, but more of a buying club) rather than just paying out of pocket.

Insurance companies are increasingly showing higher profits under Obamacare. United Health Group, the country's largest insurer, saw its stock price rise 375% since the day Obamacare became law. (Source: The Center For Public Integrity.) Many of these profits are obtained at the expense of small businesses; that same article said small business employers are dropping health care plans (forcing people to buy them through the health care exchanges) because the insurance plans are increasingly unaffordable for employers.

Health care, in that sense, is an indirect tax: providing it through your employer (it is the only form of insurance we routinely get through our jobs rather than on the open market) is an indirect tax: forcing your boss to pay $2,000 a month for you means your boss can't pay you $2,000 a month directly, and your insurance options, such as they are, are limited by your boss' payroll rather than your own financial or medical needs.

As insurance becomes more common, health care charges continue to increase. Health insurance is provided for a market unlike any other. When you buy homeowners' insurance, the insurance company looks at the cost of your home, the age of your home, and special factors to determine how risky you are (one insurance company would not insure us because we have large trees in our yard, which poses a risk of a tree falling onto your house.) When you buy car insurance, they look at your car and your age and your driving record and determine how risky you are. When you buy legal malpractice or other errors & omissions insurance, the time that you have been practicing, past claims, size of your firm, and area and nature of practice determine your premiums, based on how risky you are.

When you buy health insurance, you don't even get a physical: when you joined your company, nobody asked you much about your health risks to determine what your premium would be.

When you make a claim on auto or home or legal insurance, you can help choose your provider: I have a mechanic who handles repairs on my car, and a lawyer who defends our firm against claims. When you have a health care emergency, you don't choose your provider. Most people don't have much say in their provider, period.

Nothing about health insurance, or the health care 'marketplace', operates in any manner like any other industry where we can assert that there is relatively free and open choice. Individuals have far less information about health care costs and benefits, and far fewer choices about their options, than in any other product or service. Options are determined almost exclusively by random chance, location, and your family history.

We have single-payer education: the government provides education, and where you go to school depends largely on where you live. We have single-payer delivery services (the US Post Office). The prices you pay are dependent solely on how much you want to use, and are heavily subsidized. We have single-payer highway systems.

We have the government control or mandate those things when they are (a) very important to the public good -- education and package and letter delivery and transportation -- and (b) not easily priced via the open market. In other words, when everyone generally needs something and it's hard to have it provided privately at a reasonable cost, the government provides a public option and private companies are free to provide alternate versions.

The existence of public schools has not in any way hampered the growth of private schools. The existence of a post office has not in any way hampered the growth of delivery services and the Internet.

Until we have a public option single-payer health care system, people will inevitably become poorer and less healthy, and receive worse care, than they would otherwise. Providing a public option would not drive private care out of existence, but it might provide better care for people who are slowly being squeezed to death by higher costs of health care. Only we will not provide a public option, ever, because our health care system was broken permanently by Obamacare, and our political system no longer works. Possibly when people start dying in the streets again, or the next financial crisis hits by 2017, we will get the revolution -- it can be peaceful -- that we need.

3 comments:

I don't think it's fair to blame that on Obamacare. Obamacare is the first step toward a single-payer system. It's just that, as should have been expected, companies are taking advantage of Obamacare to raise prices and employers are using it as an excuse to raise deductibles. Neither of these things are the fault of Obamacare.

AND, because the Republicans spent their time doom and glooming it, they made everyone expect the prices to go up, so, when they did, people blame Obamacare when it's human greed that's actually doing it.

The same thing will happen when we raise the national minimum wage. Prices everywhere will go up, not because they should or need to but because employers will not want to give up any of their profits to pay their employees a living wage. So should we not raise the minimum wage because of that? That's what the Republicans are saying. But they are just providing the future excuse for corporations to raise prices.

Minimum wage is a more complicated thing. But with Obamacare, the problem lies in the fact that there is nothing preventing that kind of costly abusive behavior -- the same way there is no way to prevent the kind of costly abusive behavior colleges are engaging in. There are no price controls on medical procedures and no laws regarding how much the deductibles or copays can be. In most cases people still do not have the right to shop for insurance: you generally cannot go buy your own insurance unless your employer doesn't offer it (and if you were to opt out of employer-provided coverage and buy your own, you will likely NOT be paid the money to cover it, because the employer pays a base premium and will not give you a raise.)

One problem, then, is that there is no low-cost alternative for people. They have to have insurance, which means getting it through their employer. In that sense there is a principal-agent problem: the person paying for the services is not the one getting the services, so prices are disconnected.

If people could opt out of the private system, the way they can opt out of private schools, by taking advantage of a public system, that would remove Medicare/Medicaid from the private-funding problem (those are huge profit centers for insurers) and would provide some competition with private providers. This hasn't worked well in education at the higher-ed level because student loans change the market, but it works fairly well in public education at the K-12 level, where the average cost of private high school is $13,030 per year; that's roughly comparable to the share of property taxes that goes to funding high schools in affluent communities. There are no guaranteed student loans for private high school or elementary school, so people have to make a decision on whether the education is worth it.

As for minimum wage, having a minimum wage applicable to all workers and all jobs is foolish. There's no reason a 17-year-old should be paid the same as a 35-year-old, and no reason that line cooks are paid the same minimum as factory workers. Minimum wage laws should only be applicable to adults who are not living with someone that pays most of their expenses; and should only be applicable to people who work more than 1/2 time each week. There should also be the ability to apply for an exemption from minimum wage, based on market conditions.

But beyond that, you're right that in most cases prices would go up, because companies won't take less profit. There may not be that kind of price elasticity in many markets, though, in which case you would probably expect total jobs to go down or some companies to go out of business.

There's no perfect solution to any complex economic problem, but the Obamacare model isn't a very good one. I thought it would be better, but in the end I think we'd have been better off not passing it, as it removed any incentive to further work on the problem.

Well, I want to respond more to this, but I haven't had time, and it doesn't look like I will get time while I'm still remembering what I want to say.

Oh, well...

I don't disagree with you.

Which is not to say I completely agree, either.

I do think, though, that we are due for a new revolution.

You should read 'The Fourth Turning.' I bet you would like it.

Post a Comment